Fair Debt Collection Practices Act

If you owe money to creditors, you may be familiar with debt collectors and their persistent collection efforts. While debt collection agencies have the right to collect debts, they must follow specific debt collection laws. The Indiana Fair Debt Collection Practices Act is a federal law that provides important protections for consumers against unfair debt collection practices. Understanding these protections can help you assert your legal rights and stop abusive collection activity.

Contact us today at (317) 759-1483 to schedule your free consultation and learn how we can help protect your rights under the Indiana Fair Debt Collection Practices Act.

What Is The Fair Debt Collection Practices Act?

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects consumers from abusive debt collectors. This law works in full force alongside Indiana state law to regulate how third-party collectors and collection agencies can legally collect debts.

The FDCPA sets strict guidelines about how and when debt collectors can contact you, what they must tell you about the debt, and what practices are legally allowed.

The FDCPA applies specifically to third-party debt collectors and collection agencies, not original creditors. This means if you owe money directly to a credit card company and they attempt to collect, different rules apply. However, if your unpaid debt gets sold or transferred to a debt collection agency, the FDCPA protects you from unfair practices.

Under the law, debt collectors in Indiana must:

- Send written notice within five days of first contact detailing the amount owed and the original creditor

- Verify the debt if you dispute it in writing

- Stop contacting you if you request it in writing

- Be truthful about who they are and the debt they’re trying to collect

- Follow specific rules about when and how they can contact you

The FDCPA also requires debt collectors to provide specific information about your right to dispute the debt and request verification. If you request verification, the collection agency must pause all collection attempts until they provide it.

Common Violations of The Fair Debt Collection Practices Act

While the FDCPA establishes clear rules for collection practices, many collection agencies regularly violate these regulations in their attempts to collect debts. Understanding these common violations can help you recognize when a debt collector is breaking the law and take appropriate legal action to protect your rights.

Harassment and Abuse

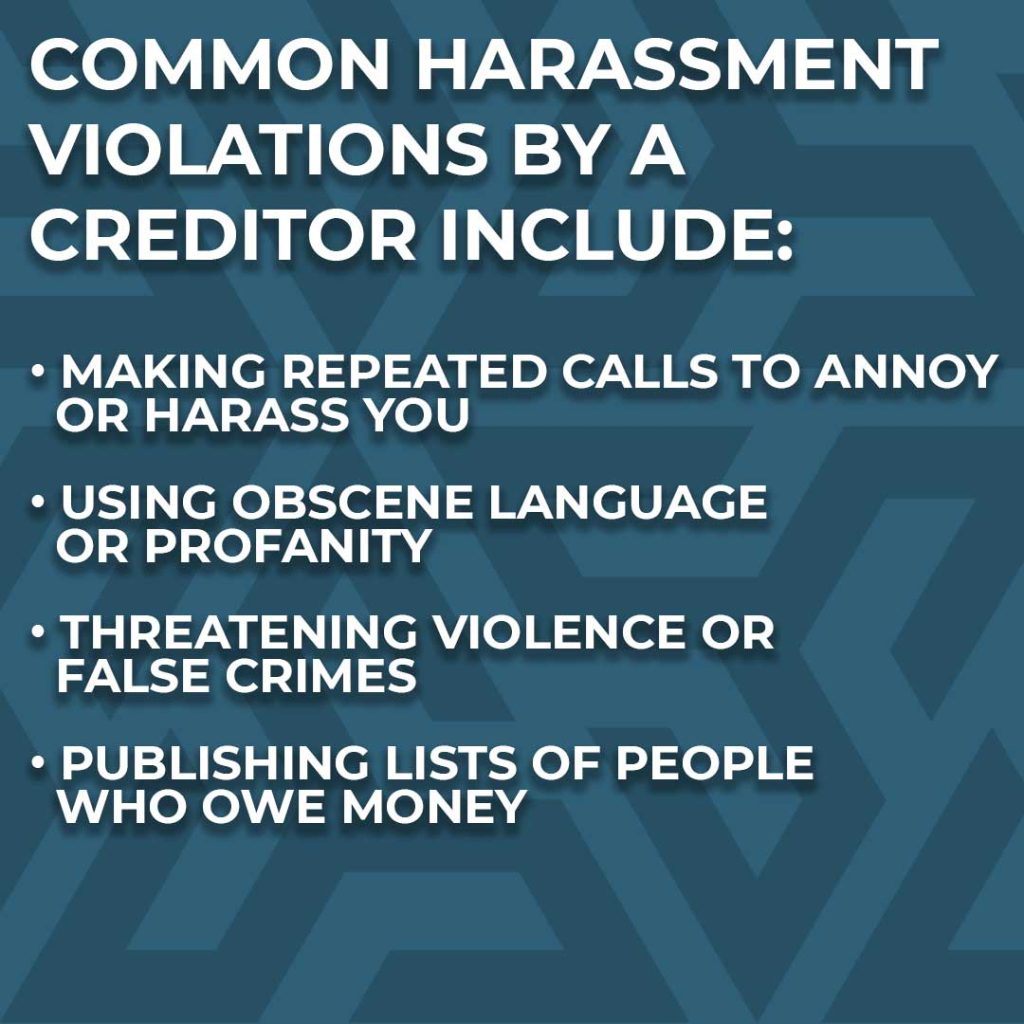

Debt collectors frequently violate the law through harassment. When a person owes money, some collectors resort to intimidation tactics that cross legal boundaries.

Common harassment violations by a creditor include:

- Making repeated calls to annoy or harass you

- Using obscene language or profanity

- Threatening violence or false crimes

- Publishing lists of people who owe money

- Calling without identifying themselves as a debt collector

- Making threats about property seizure without legal authority

- Using constant calls to pressure you to pay money

False or Misleading Information

Indiana collection agencies cannot engage in deceptive practices.

Many FDCPA violations involve collectors who:

- Misrepresent the amount you owe

- Falsely claim to be attorneys or legal representatives

- Threaten legal action they can’t or won’t take

- Provide false information about your debt to anyone

- Claim you committed a crime because you didn’t pay a debt

- Lie about the status of your debt

- Misrepresent the process or potential consequences

- Hide their identity as debt collectors

- Make false statements about bankruptcy implications

Unfair Practices

The law prohibits debt collectors from using unfair practices to collect debts.

Common violations include:

- Adding unauthorized fees or interest

- Threatening wage garnishment without a court order

- Contacting you at inconvenient times (before 8 AM or after 9 PM)

- Discussing your debt with your employer or others

- Attempting to collect debts discharged in bankruptcy

- Refusing to verify disputed debts

- Depositing post-dated checks before the agreed date

- Making false threats about your credit report

- Attempting to collect more than legally owed

- Using unjust practices to coerce payment

Contact Restrictions

Collectors violate the FDCPA when they disregard contact restrictions in Indiana, such as:

- Continuing contact after you request them to stop in writing

- Contacting you directly when they know you have an attorney

- Contacting you at work if they know your employer prohibits such calls

- Communicating with third parties about your debt except to gather location information

- Contacting you during inconvenient hours

- Ignoring cease communication requests

- Discussing your employment or financial situation with others

What You Can Do if a Debt Collector Breaks the Law in Indiana

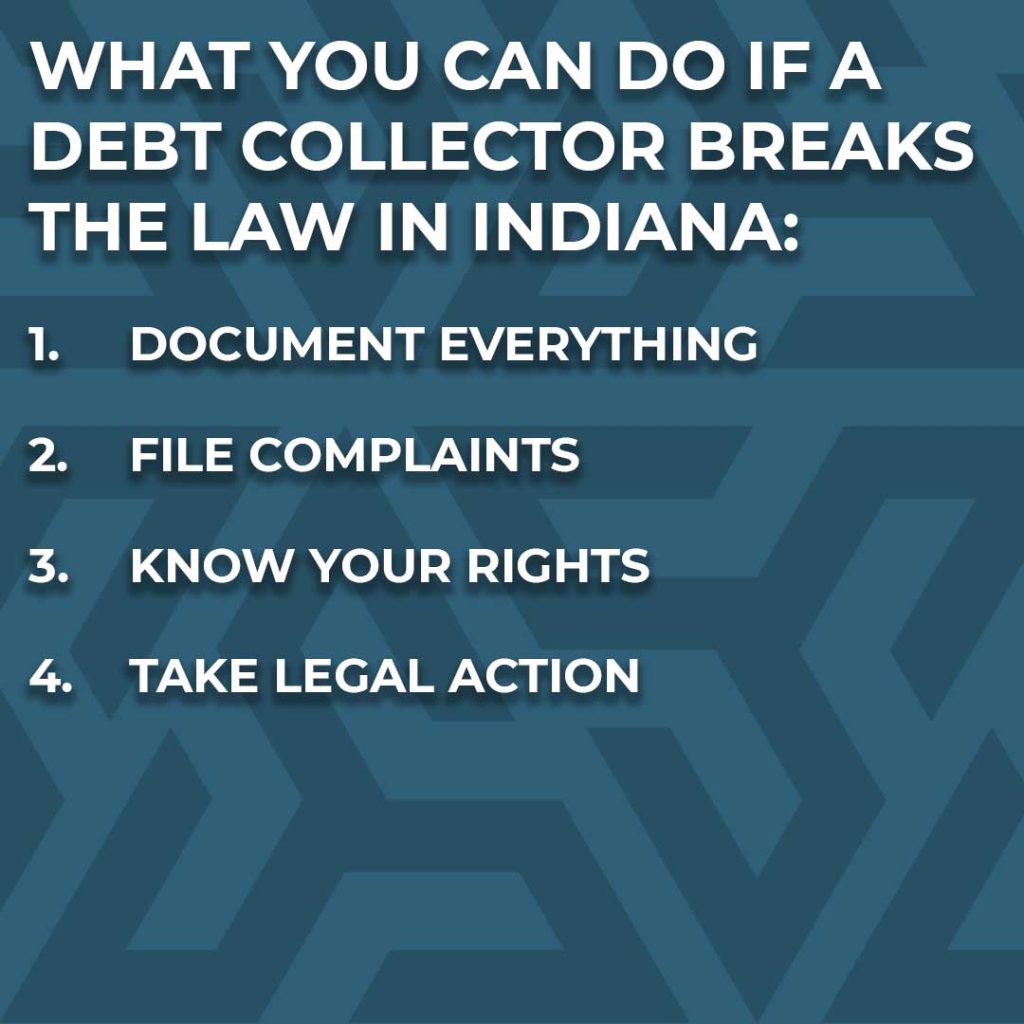

If you believe a debt collector has violated your legal rights under Indiana law, you have several options to protect yourself and seek justice:

Document Everything

Keep detailed records of all interactions with debt collectors. This includes recording dates, times, and content of all calls while saving all letters and written communications. Be sure to note the names of collectors and their agencies, and document any witnesses to harassment that occurs.

It’s also important to keep records of your employment situation if relevant to your case, along with any evidence of illegal collection activity. Finally, maintain careful documentation of any financial losses you’ve suffered due to FDCPA violations, as this information may be crucial for your Indiana case.

File Complaints

Multiple agencies can help address FDCPA violations, and you should take advantage of all available reporting channels. Start by submitting complaints to the Indiana Attorney General and reporting violations to the Federal Trade Commission.

Filing a complaint with the Consumer Financial Protection Bureau and connecting with your local consumer protection office in Indiana is also recommended. Consider reporting violations to relevant industry associations as well. Throughout this process, be sure to document all complaint submissions and responses, as these records may prove valuable for your case.

Know Your Rights

Understanding your rights is crucial when dealing with Indiana debt collectors. You have the fundamental right to dispute the validity of the debt and request debt verification. The law protects your right to demand collectors stop contacting you, and you always maintain the right to seek representation.

Additionally, you have the right to sue for violations of consumer protection laws and to be protected from unjust practices. Perhaps most importantly, you’re entitled to receive accurate information about your debts, and Indiana collectors must honor these legal rights throughout the collection process.

Take Legal Action

If a debt collector violates the law, you may be entitled to significant remedies through the legal system. These can include statutory damages up to $1,000 per violation, as well as actual damages for any financial losses you’ve suffered.

The law also provides for payment of attorney fees and compensation for emotional distress caused by illegal collection practices.

Federal courts can issue orders stopping illegal collection practices, and in some cases, you may be awarded punitive damages. Additionally, you might be entitled to cancellation of illegally inflated debts that resulted from unfair collection practices.

The process can help you obtain justice and hold debt collectors accountable for unjust practices. However, navigating debt collection laws requires experience in both Indiana law and federal regulations. An experienced attorney can help you understand your options and protect your rights.

Frequently Asked Questions About Debt Collection in Indiana

What exactly protects consumers from unfair debt collection practices?

Both federal law and Indiana state law protect abusive collection efforts. The FDCPA specifically regulates how debt collectors and debt collection agencies can interact with consumers, setting clear boundaries for what is legally allowed for debt collector attempts.

Can a debt collector or collection agency call me at any time?

No. By federal law, debt collectors are restricted in when they can make calls. An Indiana collection agency cannot contact a person before 8 AM or after 9 PM, and they must stop calling if you request it in writing. They also cannot call you at work if your employer prohibits such calls.

What should I do when a debt collection agency first contacts me?

When a debt collector first contacts you, they must send a letter within five days detailing the debt amount and the original creditor. Review this information carefully and consider requesting debt verification before making any payments to creditors.

Can filing bankruptcy stop debt collection attempts?

Yes. When filing a bankruptcy case, an automatic stay goes into effect that requires all creditors and debt collectors to immediately cease their collection efforts. This protection under federal law remains in place while your bankruptcy case proceeds through the courts and becomes permanent upon your discharge.

What information are debt collectors or creditors not legally allowed to share in Indiana?

Debt collectors cannot discuss your debt with anyone except you, your spouse, or your attorney. They cannot tell your employer, neighbors, or family members about your debt, though they may get in touch with these people once to locate you.

Do I need an attorney to deal with debt collection violations?

While not required, having an attorney is highly recommended when dealing with violations by creditors. An experienced attorney can help document violations, negotiate with the collection agency, and ensure your rights are protected throughout the process.

What should I do if I believe a debt collector has violated my rights?

First, document the incident in detail, including dates, times, and what occurred. Keep any voicemails, letters, or other evidence. Then, consider consulting with an attorney who can help you understand your options and potentially file a complaint or lawsuit against the creditors.

Can debt collectors add fees to my original debt?

Debt collectors can only add fees that were authorized in your original agreement with the creditor or that are specifically allowed by law. Any unauthorized fee constitutes a violation of debt collection laws.

What if I don’t believe I owe the debt?

In Indiana, you have the right to dispute any debt and request verification. Send a written dispute letter to the collection agency within 30 days of receiving their initial notice. They must then cease collection activities until they provide verification of the debt.

Can debt collectors threaten to have me arrested?

No. It’s illegal in Indiana for debt collectors to threaten arrest or criminal prosecution for unpaid consumer debts. If a collector makes such threats, they are in violation of the law and a person should document this behavior and report it to the appropriate authorities and possibly take them to court.

Contact Sawin & Shea for Violations of The Indiana Fair Debt Collection Practices Act

When dealing with aggressive debt collectors or unfair collection practices, a person needs experienced attorneys who understand both the FDCPA and Indiana law. The team at Sawin & Shea has helped countless clients stand up to abusive collection agencies and protect their rights in and out of court.

Our attorneys can help with a comprehensive range of debt collection issues. We excel at stopping harassment from debt collectors and fighting unfair collection practices that violate your rights. Our team has extensive experience handling bankruptcy cases and defending against illegal collection efforts. We’re skilled at recovering damages for FDCPA violations while protecting debtors from unjust practices throughout the process.

Whether you need help resolving disputes with collection agencies or ensuring fair treatment under the law, our experienced team is prepared to advocate for your rights and interests.

We understand the challenges individuals face when dealing with debt collectors. Whether you’re considering bankruptcy, facing wage garnishment, or experiencing harassment, our team can help. Our experience with both the FDCPA and Indiana law allows us to provide comprehensive protection for our clients.

When consumers work with Sawin & Shea, you get experienced attorneys who know debt collection laws inside and out, along with strategic guidance tailored to your specific situation. We provide comprehensive protection from illegal collection practices while maintaining clear communication about your rights throughout the process.

Our Indiana firm delivers aggressive representation in and out of court against violators of debt collection laws, coupled with unwavering support throughout the legal process. Above all, we maintain a steadfast dedication to achieving the best possible outcome for each of our clients.

Don’t let debt collectors bully you or violate your rights. If you’ve experienced harassment, false claims, or other unjust practices by a creditor, you have options. Our team can help you understand your rights and take action in court to protect yourself.

Our attorneys will evaluate your case, explain your rights, and help you fight back against unfair collection practices by a creditor. We’ve helped numerous people in Indiana obtain justice and protection under the law, and we’re ready to put our experience to work for all consumers.

Call Sawin & Shea today at (317) 759-1483 for a free consultation.