Rising healthcare costs are continually leaving thousands of Americans drowning in medical debt. In fact, medical debt is one of the most common types of debt reported on consumer credit reports.

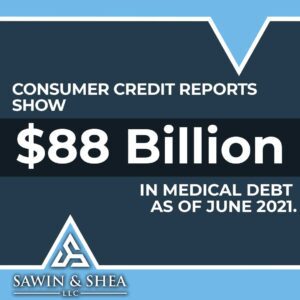

According to the Consumer Financial Protection Bureau, consumer credit reports show $88 billion in medical debt as of June 2021. However, it is expected that medical debts are much higher since not all medical debts are furnished to consumer reporting agencies.

Because of the serious burden medical debts have placed on Americans, many are turning to bankruptcy as a potential option. However, while bankruptcy can help, it’s important to understand how the process works, especially concerning your medical debt.

At Sawin & Shea, our team of Chapter 7 and Chapter 13 bankruptcy lawyers is here to help. We understand how stressful even just considering bankruptcy can be and are dedicated to providing quality, compassionate representation to help you through this trying time.

Can You File Bankruptcy on Medical Bills?

Simply put, yes, you can file bankruptcy on your medical bills. Your medical bills are considered “unsecured debts” which means there is no property that can be taken from you under contract as a result of not paying your medical bills — and most unsecured debts, like medical bills, are eligible for bankruptcy.

Medical debts are also considered a necessity, which means they are protected under the “necessity” doctrine. In other words, because medical debts typically come from paying for treatment that is considered a life necessity, they cannot be subjected to fraud or luxury purchase analysis. Thus your right to have your medical debts discharged will not be taken away.

Does Bankruptcy Clear Medical Debt?

How your medical debts are discharged or if they are fully discharged will depend on the type of bankruptcy you file.

Chapter 7 Medical Debts & Bankruptcy

If you file Chapter 7, you can have your medical debts discharged or wiped away, however, there is a caveat. In Chapter 7, certain non-exempt assets can be used to pay off your debts. Some of your property will be exempt, such as your personal property and necessities.

However, each state has a statutory structure that determines what assets you can hold onto thoroug the bankruptcy process. Non-exempt items could be taken, liquidated, and the proceeds used to help pay your creditors something.. If you have any assets you are worried about losing, consult a bankruptcy attorney who can talk to you about what you can hold onto in a Chapter 7. Chapter 7 may not aways be the best option, but it is a way to have all of your medical debts cleared.

Chapter 13 Medical Debts & Bankruptcy

Chapter 13 bankruptcies work by setting up a three- to five-year payment plan so you can make more affordable payments based on what the law says you have to pay under a couple of tests. In these cases, your assets and property are protected and will not be taken from you, but you will still be required to make a payment on your debts. What you have to pay is a function of an asset based test and an income based test. Many Chapter 13 Debtors pay pennies on the dollar back to their unsecured creditors.

After you have completed your Chapter 13 payment plan, if there is any remaining unsecured debt, it will be discharged with a few exceptions like some taxes, most student loans, and child support. This is the better option if you want to protect your assets, or if you are otherwise not eligible for a Chapter 7 case.

How to Qualify for Bankruptcies

If you intend to file bankruptcy for your medical debts, you will need to meet certain requirements. For Chapter 7 the requirements are as follows:

- Your average monthly income from the past six months must be lower than the median income for your household size in your state. You may also need to take a means test to determine whether your disposable income is high enough to make partial payments.

- You haven’t filed for Chapter 7 bankruptcy in the past eight years.

- You haven’t filed for Chapter 13 bankruptcy in the past six years.

For Chapter 13 bankruptcy, the following are the requirements:

- You have sufficient income to make the payments outlined in your bankruptcy plan.

- Your combined total secured and unsecured debts are less than $2,750,000.

- You can provide proof of filing your federal and state tax returns for the past four years.

How Sawin & Shea, LLC Can Help

At Sawin & Shea, we believe in providing compassionate and understanding representation to those struggling with debt. We understand how stressful and even confusing filing for bankruptcy can be. Our bankruptcy attorneys have years of experience in bankruptcy cases, including those involving medical debts, and can help walk you through the process every step of the way. We can even offer guidance after your bankruptcy case has ended.

Contact us at 317-759-1483 or send us an email for a free consultation today!